2012-05-23 22:07:07

πηγή: Social Europe journal

BY MARSHALL AUERBACK

The escalating run on the banks on Europe’s periphery is now front page news. Even the Germans no doubt realize that moving on a scale great enough to arrest such a bank run will risk potential Target 2 losses on a huge scale. The odds are some kind of huge ECB efforts to stem this run is at hand. If not, they risk a fully fledged banking collapse.

The European System of Central Banks (ESCB) is quite complex. The “backdoor” lender of last financing of the banks in the PIIGS that are losing deposits through the ECB is less than transparent. In spite of its complexities, the ECB can move quickly to arrest this problem. Of all the financial maladies that exist, the one with which the world has the most experience and therefore has developed the most effective tools to address is a bank run.

It is therefore a bit of a puzzle why one of the most commonly cited fears about a Greek departure from the Eurozone is that it would lead to a bank run in other Eurozone countries

. The reason for the fears, as with all things European, is that politics prevents a common sense response. Politics is an obstacle, but in that panicked weekend in the future when the powers that be are worried about what might happen on Monday morning, all of the theoretical political obstacles that had prevented action will be forgotten. The points are obvious ones, but sometimes it is useful to reiterate the obvious in order to identify the real risks that exist in as complicated a set of circumstances as a Greek departure from the Eurozone might entail.

The obvious point to make is that deposit insurance is a proven cost-effective way of limiting downside risk in a financial meltdown. Bank runs are liquidity problems, not solvency problems. This is important because insolvent institutions rarely fail as long as they are liquid. Thus, it is not necessary to restore the solvency of an institution when a bank run develops and incur all the trouble and expense that this entails. All one need do is reassure depositors that they have access to their money. Moreover, keeping deposits in a bank eliminates the need to liquidate the asset side of the balance sheet at fire sale prices. Even a normally solvent institution can become insolvent if it were forced to liquidate its assets too rapidly.

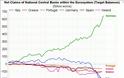

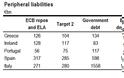

The run on the banks on Europe’s periphery is already huge and is accelerating. In a FT article Gavyn Davies provided a table and a chart that illustrate this point.

And from David Mackie at JP Morgan:

The table reflects March or April data and the chart reflects mid Q1 2012 data. Target 2 refers to Trans-European Automated Real-time Gross Settlement Express Transfer. It is the euro system’s operational tool through which the national central banks of member states provide payment and settlement services for intra/euro area transactions. Target 2 claims can arise from trade and current account transactions as well as purely financial transactions. Recently financial transactions have become dominant. Funds have been taken out of banks on Europe’s periphery and have been deposited in banks in the north of Europe, principally in Germany. The bank receiving the deposit has its funds delivered through the national central banks to the bank on the periphery that has lost deposit funds. That is a Target 2 transaction. The so-called Target 2 outstanding balance is the net position of such claims between two European countries.

ELA stands for Emergency Liquidity Assistance. Such assistance is extended by single national central banks to their banking systems. The risk is borne at the national level. The collateral requirements imposed upon a commercial bank for obtaining ELA funds is less than the collateral requirements needed for obtaining Target 2 funds. However, though I am not absolutely sure of this, the national central bank in a country like Greece with commercial bank deposit runs – ultimately funds its ELA financial assistance to its commercial banks from the ECB.

In a recent Bloomberg article, it was suggested that the deposit runs from Greece, Ireland, and Portugal combined to date have been equal to 52% of the original pre-run deposits. I suddenly realized that, if the first two columns in the above table were additive, the total deposit runs from these two banks could be half of all original deposits. Why? Put very simply, the sum of “ECB repos and ELA” and “Target 2” for Greece, Ireland, and Portugal in the above table is 606 billion euros and the sum of the remaining bank deposits in these same countries is 596 billion euros. If the first two columns in the above table correspond to total lender of last resort financing, which should be roughly equal to the total deposit run as of that date, that run of 606 billion euros is roughly equal to 52% of the original deposit position (today’s outstanding deposits of euro 596 billion plus the total such “flight” deposits of euro 606 billion.)

How can that be? The total deposit run from the banks of Greece, Ireland, and Portugal must no doubt exceed the Target 2 and ELA financing, since some of those deposit funds surely went to banks outside the euro area like the Swiss banks and dollar-based banks. If the flight of deposits went to such non euro banks in large measure, that part of the deposit run would have forced closure of banks in Greece, Ireland, and Portugal unless they received lender of last resort financing from the ECB. Such lender of last resort financing would be above and beyond total Target 2 and ELA financing. That is probably the source of the ECB repo financing in the above table.

We can see from the above chart that Portugal, Ireland, Greece, Italy and Spain have been losing deposits and most of these deposits have gone into German banks. The flight deposit funds that have gone into German banks have been recycled back to the banks on the periphery through Target 2 and the associated ELA (Emergency Liquidity Assistance). For now let’s not worry about the institutional details.

Most commentators estimate the run on the Greek banks to date is equal to about a third of the original Greek bank deposits. The above table suggests the deposit loss is larger. It would seem from this table that the Greek deposit flight into euro area banks has been over 40% of the original deposits. From what I can tell the Greek flight deposit funds recycled back through the ECB and ELA may be more than is reflected in this table. In addition there have no doubt been additional deposit losses that have gone into dollar, Swiss franc, and other non euro system banks.

In other words, the deposit run to date on Greece has been enormous. The same could be said of the Irish banks.

So far the deposit losses from Italian and Spanish banks are a much smaller share of the original outstanding deposit liabilities. However, these deposit runs have accelerated greatly through the end of April, prior to the Greek and French elections. For Spain the Target 2 claims due to deposit runs has gone from a little more than 10% of Spanish GDP at year end 2011 to almost 30% of GDP by the end of April. For Italy these same numbers have gone from roughly 10% of Italian GDP at the end of 2011 to 20% at the end of April. Based on the Greek precedent, these deposit runs could become much larger in a fairly short time now that there is a heightened concern about a possible euro exit of all these peripheral countries or alternatively a German exit from the euro.

These Target 2 and ELA flows are part of an established ECB lender of last resort mechanism. The rules allow for this kind of lender of last resort financing of deposit runs up to certain collateral limits. Without going into the details, it seems to me that there could be another 40% run on the remaining Greek bank deposits before these collateral limits are reached. In other words, under the current ECB rules all of these countries could have ECB lender of last resort financing and deposit runs up to perhaps 60% of their original deposits. That would constitute an aggregate deposit run of almost three trillion euros from the five PIIGS.

As a consequence, the system of European central banks would be on the hook for losses, possibly from exchange devaluation if all these five peripheral countries left the euro, of some substantial percentage of a euro three trillion liquidity finance exposure. Almost everyone assumes that the Germans will not allow this liquidity financing of deposit runs on the periphery to proceed. They will stop such financing. The Germans will opt out of the euro.

In Gavyn Davies’ article he says:

As the table (from David Mackie of J.P. Morgan) shows, the outstanding bank deposits of the periphery are many times larger than the current exposures of the ECB and core governments to the periphery. It seems inconceivable that core countries like Germany will be willing to expose themselves to these risks if the deposit flight continues.

I disagree. I believe the Germans are trapped. They almost cannot and in fact will not stop this deposit run if it continues up to the collateral rule limit. Why?

To stop such lender of last resort lending as long as there is adequate collateral would be to abrogate ECB procedures and rules and, in doing so, cut off liquidity financing to banks experiencing runs. This would force those banks to suspend deposit withdrawals. The failure of the ECB to perform its lender of last resort role in any one of these countries would immediately accelerate deposit runs in other European countries. This could extend beyond the five PIIGS to France and other countries. I do not believe any German government officials or ECB bureaucrats would take responsibility for such an outcome, even if they had the authority.

I believe that a German exit from the ECB to limit such Target 2 loss exposure is even less likely. Germany is bound by a treaty. Any move to exit would require some kind of debate and possibly a referendum in Germany. On the first move in such a direction a massive run would be precipitated on banks not just in the five distressed peripheral countries but in other countries including France as well.

Although all the flight deposit funds are going into German banks, under the ECB rules Germany’s loss exposure is limited to its 28% participation in the ECB. Were Germany to exit the euro its banking system including the Bundesbank might be exposed to almost all of such losses rather than the mere 28% under the current euro system.

Lastly, any such German euro exit could cause its new exchange rate to soar which would be very adverse to its large international trade exposure. Furthermore, any such move that brought calumny to the banks elsewhere in Europe and thereby to those economies might greatly impair German international trade relations within Europe for a long time.

The bank run is already very large and could be exploding. Germany is not in a position to either limit the run under ECB rules or exit the euro in order to contain its loss exposure to the liquidity financing of banks on the European periphery. Germany is trapped.

Gavyn Davies reports that at the G-8 meeting Italy’s Mario Monti proposed up front deposit insurance rather than “backdoor” Target 2 and ELA financing to deal with Europe’s bank run.

Mario Monti apparently took a plan to the G8 summit to offer jointly-funded guarantees on bank deposits to apply across the entire eurozone. This would certainly help, but whether it would be sufficient to eliminate fears of exchange rate losses if the euro were to disintegrate is another matter. To fix that problem, belief in the integrity of the euro as a single currency needs to be restored. The bank run could bring matters to a head.

Because Germany is trapped, I believe that Europe including Germany will go this route.

As Gavyn Davies says, for such deposit insurance to succeed will require lesser “fears of exchange rate losses if the euro were to disintegrate”.

youpayyourcrisis

BY MARSHALL AUERBACK

The escalating run on the banks on Europe’s periphery is now front page news. Even the Germans no doubt realize that moving on a scale great enough to arrest such a bank run will risk potential Target 2 losses on a huge scale. The odds are some kind of huge ECB efforts to stem this run is at hand. If not, they risk a fully fledged banking collapse.

The European System of Central Banks (ESCB) is quite complex. The “backdoor” lender of last financing of the banks in the PIIGS that are losing deposits through the ECB is less than transparent. In spite of its complexities, the ECB can move quickly to arrest this problem. Of all the financial maladies that exist, the one with which the world has the most experience and therefore has developed the most effective tools to address is a bank run.

It is therefore a bit of a puzzle why one of the most commonly cited fears about a Greek departure from the Eurozone is that it would lead to a bank run in other Eurozone countries

The obvious point to make is that deposit insurance is a proven cost-effective way of limiting downside risk in a financial meltdown. Bank runs are liquidity problems, not solvency problems. This is important because insolvent institutions rarely fail as long as they are liquid. Thus, it is not necessary to restore the solvency of an institution when a bank run develops and incur all the trouble and expense that this entails. All one need do is reassure depositors that they have access to their money. Moreover, keeping deposits in a bank eliminates the need to liquidate the asset side of the balance sheet at fire sale prices. Even a normally solvent institution can become insolvent if it were forced to liquidate its assets too rapidly.

The run on the banks on Europe’s periphery is already huge and is accelerating. In a FT article Gavyn Davies provided a table and a chart that illustrate this point.

And from David Mackie at JP Morgan:

The table reflects March or April data and the chart reflects mid Q1 2012 data. Target 2 refers to Trans-European Automated Real-time Gross Settlement Express Transfer. It is the euro system’s operational tool through which the national central banks of member states provide payment and settlement services for intra/euro area transactions. Target 2 claims can arise from trade and current account transactions as well as purely financial transactions. Recently financial transactions have become dominant. Funds have been taken out of banks on Europe’s periphery and have been deposited in banks in the north of Europe, principally in Germany. The bank receiving the deposit has its funds delivered through the national central banks to the bank on the periphery that has lost deposit funds. That is a Target 2 transaction. The so-called Target 2 outstanding balance is the net position of such claims between two European countries.

ELA stands for Emergency Liquidity Assistance. Such assistance is extended by single national central banks to their banking systems. The risk is borne at the national level. The collateral requirements imposed upon a commercial bank for obtaining ELA funds is less than the collateral requirements needed for obtaining Target 2 funds. However, though I am not absolutely sure of this, the national central bank in a country like Greece with commercial bank deposit runs – ultimately funds its ELA financial assistance to its commercial banks from the ECB.

In a recent Bloomberg article, it was suggested that the deposit runs from Greece, Ireland, and Portugal combined to date have been equal to 52% of the original pre-run deposits. I suddenly realized that, if the first two columns in the above table were additive, the total deposit runs from these two banks could be half of all original deposits. Why? Put very simply, the sum of “ECB repos and ELA” and “Target 2” for Greece, Ireland, and Portugal in the above table is 606 billion euros and the sum of the remaining bank deposits in these same countries is 596 billion euros. If the first two columns in the above table correspond to total lender of last resort financing, which should be roughly equal to the total deposit run as of that date, that run of 606 billion euros is roughly equal to 52% of the original deposit position (today’s outstanding deposits of euro 596 billion plus the total such “flight” deposits of euro 606 billion.)

How can that be? The total deposit run from the banks of Greece, Ireland, and Portugal must no doubt exceed the Target 2 and ELA financing, since some of those deposit funds surely went to banks outside the euro area like the Swiss banks and dollar-based banks. If the flight of deposits went to such non euro banks in large measure, that part of the deposit run would have forced closure of banks in Greece, Ireland, and Portugal unless they received lender of last resort financing from the ECB. Such lender of last resort financing would be above and beyond total Target 2 and ELA financing. That is probably the source of the ECB repo financing in the above table.

We can see from the above chart that Portugal, Ireland, Greece, Italy and Spain have been losing deposits and most of these deposits have gone into German banks. The flight deposit funds that have gone into German banks have been recycled back to the banks on the periphery through Target 2 and the associated ELA (Emergency Liquidity Assistance). For now let’s not worry about the institutional details.

Most commentators estimate the run on the Greek banks to date is equal to about a third of the original Greek bank deposits. The above table suggests the deposit loss is larger. It would seem from this table that the Greek deposit flight into euro area banks has been over 40% of the original deposits. From what I can tell the Greek flight deposit funds recycled back through the ECB and ELA may be more than is reflected in this table. In addition there have no doubt been additional deposit losses that have gone into dollar, Swiss franc, and other non euro system banks.

In other words, the deposit run to date on Greece has been enormous. The same could be said of the Irish banks.

So far the deposit losses from Italian and Spanish banks are a much smaller share of the original outstanding deposit liabilities. However, these deposit runs have accelerated greatly through the end of April, prior to the Greek and French elections. For Spain the Target 2 claims due to deposit runs has gone from a little more than 10% of Spanish GDP at year end 2011 to almost 30% of GDP by the end of April. For Italy these same numbers have gone from roughly 10% of Italian GDP at the end of 2011 to 20% at the end of April. Based on the Greek precedent, these deposit runs could become much larger in a fairly short time now that there is a heightened concern about a possible euro exit of all these peripheral countries or alternatively a German exit from the euro.

These Target 2 and ELA flows are part of an established ECB lender of last resort mechanism. The rules allow for this kind of lender of last resort financing of deposit runs up to certain collateral limits. Without going into the details, it seems to me that there could be another 40% run on the remaining Greek bank deposits before these collateral limits are reached. In other words, under the current ECB rules all of these countries could have ECB lender of last resort financing and deposit runs up to perhaps 60% of their original deposits. That would constitute an aggregate deposit run of almost three trillion euros from the five PIIGS.

As a consequence, the system of European central banks would be on the hook for losses, possibly from exchange devaluation if all these five peripheral countries left the euro, of some substantial percentage of a euro three trillion liquidity finance exposure. Almost everyone assumes that the Germans will not allow this liquidity financing of deposit runs on the periphery to proceed. They will stop such financing. The Germans will opt out of the euro.

In Gavyn Davies’ article he says:

As the table (from David Mackie of J.P. Morgan) shows, the outstanding bank deposits of the periphery are many times larger than the current exposures of the ECB and core governments to the periphery. It seems inconceivable that core countries like Germany will be willing to expose themselves to these risks if the deposit flight continues.

I disagree. I believe the Germans are trapped. They almost cannot and in fact will not stop this deposit run if it continues up to the collateral rule limit. Why?

To stop such lender of last resort lending as long as there is adequate collateral would be to abrogate ECB procedures and rules and, in doing so, cut off liquidity financing to banks experiencing runs. This would force those banks to suspend deposit withdrawals. The failure of the ECB to perform its lender of last resort role in any one of these countries would immediately accelerate deposit runs in other European countries. This could extend beyond the five PIIGS to France and other countries. I do not believe any German government officials or ECB bureaucrats would take responsibility for such an outcome, even if they had the authority.

I believe that a German exit from the ECB to limit such Target 2 loss exposure is even less likely. Germany is bound by a treaty. Any move to exit would require some kind of debate and possibly a referendum in Germany. On the first move in such a direction a massive run would be precipitated on banks not just in the five distressed peripheral countries but in other countries including France as well.

Although all the flight deposit funds are going into German banks, under the ECB rules Germany’s loss exposure is limited to its 28% participation in the ECB. Were Germany to exit the euro its banking system including the Bundesbank might be exposed to almost all of such losses rather than the mere 28% under the current euro system.

Lastly, any such German euro exit could cause its new exchange rate to soar which would be very adverse to its large international trade exposure. Furthermore, any such move that brought calumny to the banks elsewhere in Europe and thereby to those economies might greatly impair German international trade relations within Europe for a long time.

The bank run is already very large and could be exploding. Germany is not in a position to either limit the run under ECB rules or exit the euro in order to contain its loss exposure to the liquidity financing of banks on the European periphery. Germany is trapped.

Gavyn Davies reports that at the G-8 meeting Italy’s Mario Monti proposed up front deposit insurance rather than “backdoor” Target 2 and ELA financing to deal with Europe’s bank run.

Mario Monti apparently took a plan to the G8 summit to offer jointly-funded guarantees on bank deposits to apply across the entire eurozone. This would certainly help, but whether it would be sufficient to eliminate fears of exchange rate losses if the euro were to disintegrate is another matter. To fix that problem, belief in the integrity of the euro as a single currency needs to be restored. The bank run could bring matters to a head.

Because Germany is trapped, I believe that Europe including Germany will go this route.

As Gavyn Davies says, for such deposit insurance to succeed will require lesser “fears of exchange rate losses if the euro were to disintegrate”.

youpayyourcrisis

ΦΩΤΟΓΡΑΦΙΕΣ

ΜΟΙΡΑΣΤΕΙΤΕ

ΔΕΙΤΕ ΑΚΟΜΑ

ΠΡΟΗΓΟΥΜΕΝΟ ΑΡΘΡΟ

Τι ζήτησε ο Σαμαράς στο ΕΛΚ

ΕΠΟΜΕΝΟ ΑΡΘΡΟ

Ε, ΡΕ ΓΛΕΝΤΙΑ...

ΣΧΟΛΙΑΣΤΕ